Performance Summary

Past performance is not a reliable indicator of future performance

Source: Internal CI data reports, March 31, 2025

MSCI AC World is the Fund’s Benchmark, MSCI Midcap is a reference benchmark.

Inception Date: 2 July 2019

*Annualised

$100k Invested Since Inception (net)

Past performance is not a reliable indicator of future performance

Source: Internal CI data reports, March 31, 2025

Risk/Return Since Inception (Per Annum)

Quarterly Highlights

- The Family & Founder Fund returned -0.01% for the quarter net of fees and expenses. Since inception the fund has returned 9.36% pa net of all fees and expenses.1

- The quarter saw a notable change in momentum in markets with the Nasdaq down 10% for the quarter, driving the MSCI ACWI down 2% in AUD. Small caps continued their underperformance with the MSCI AC smalls -5%, whilst MSCI AC Midcap performed better at -1%.

- European markets were positive for the quarter, also supported by a stronger currency as the Euro increased to the USD and AUD. European holdings in Aker Asa (AKER) (+20%), Heineken (HEIA) (+13%), Vivendi (VIV) (+10%) and Investor AB (INVE.B) (+6%) were positive contributors during the quarter. The Funds top performer was US company Royalty Pharma (RPRX) (+22%) as they announced the internalisation of its management company, which we discuss below. Brown & Brown (BRO) and Arthur J Gallagher (AJG) were also meaningful contributors with both +20% as the threat of tariffs and follow on inflationary impacts are seen as a positive for insurance brokers.

- Brookfield (BN), Colliers (CIGI), Alimentation Couche Tard (ATD) were the main detractors to performance during the quarter as the threat of tariffs and potential slowdown impacted the more macro sensitive areas of the portfolio.

¹ Past performance is not a reliable indicator of future performance.

Portfolio Insights & Market Observations

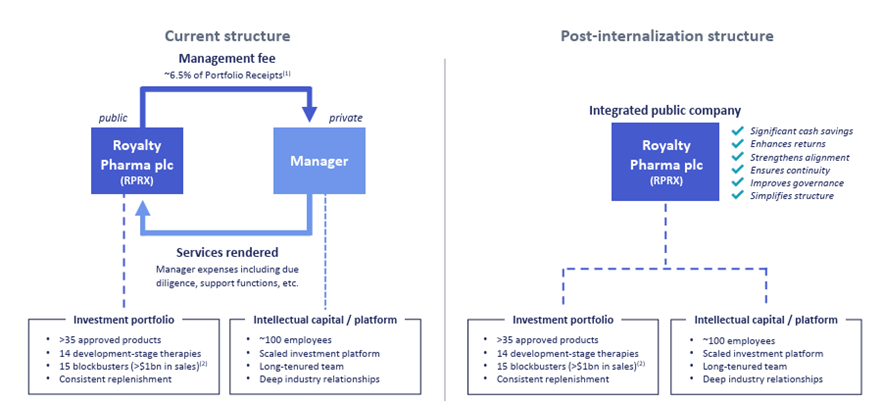

During the quarter Royalty Pharma (RPRX) announced the internalisation of its external management company. Royalty Pharma founded in 1996 by CEO Pablo Legorreta is the world’s leader in biopharmaceutical royalties. The company owns a portfolio of 35 royalties that generates cash inflows of $2.8bn pa. Royalty Pharma has been externally managed since its founding, with the external manager conducting all aspects of the business and operations, with Royalty Pharma owning the portfolio of royalties.

The company listed in 2020 at $28. Despite executing on the opportunity and growing royalty receipts from $1.7bn in 2019 to $2.8bn in 2024, the stock price was still sitting at $25 in the middle of 2024. Trading at 6x cash flows. Management had improved transparency and increased buybacks but to no avail.

The internalisation announcement is a major step forward and the shares increased 22% during the quarter off the back of the announcement. Royalty pharma is paying $1.1bn in cash and shares to acquire the manager. Year 1 savings will be >$100m in avoiding fees/costs to the manager and increasing to over $175m by 2030, making it an accretive deal for Royalty Pharma shareholders. Pablo alongside the rest of the Management and the board own 25% of Royalty Pharma. They have shown their commitment to Royalty Pharma by conducting a fair internalisation transaction (they potentially could have got more money by selling the external manager to a large alternative manager but have full commitment to Royalty Pharma). The transaction is expected to close in the next quarter.

Chart 1: Current Structure and Post Internalisation Structure of Royalty Pharma

Source: Company Reports

Ensuring Royalty Pharma has the right corporate structure for investors can be a significant long-term boost, as many investors will prefer the governance and alignment of an integrated company as opposed to one with an external manager. Royalty Pharma shares trade on a lowly 7x cash flows. They continue to acquire new royalties at attractive teens returns and grow the portfolio. During the quarter we spent time in Boston and NY meeting with the Royalty Pharma management team as well as biotechnology and life sciences industry participants. Funding in life sciences continues to be soft as the appetite for high risk, long duration investments have waned. At the same time the cost of developing a drug keeps rising with the typical trial costing >$1bn. Very few companies can afford a portfolio of these investments at a single point in time. These dynamics should see royalties continue to gain momentum as a funding source and provide further attractive investment opportunities for Royalty Pharma.

Royalty Pharma is the type of highly predictable business with value latency and A grade stewardship we are seeking more of. In 2024 the funds top performers were those exposed to the strong US economy and improving financial markets. The emergence of trade tariffs have quickly slowed this train down. The Fund sold multi-year holdings of Marriott (MAR), Lennox (LII) and Schindler Holding (SCHP) during the quarter. All three were successful investments for the fund as they have had a positive operating environment, strong management execution with advantaged business models - Lennox in the HVAC oligopoly, Schindler with its lift service portfolio while Marriott has one of the best business models we have seen with its franchise fee model. However, we see near term trends softening in all three of these businesses alongside all time high valuations and subsequently sold.

The Fund added a new position in Puig Brands (PUIG), a $10bn market cap Spanish based leader in prestige fragrances and beauty products. The company owns top tier brands of Rabanne, Jean Paul Gaultier, Carolina Herrera and Charlotte Tilbury. The company listed last year at EUR24.50 with the shares trading down since to EUR16 and 15x PE. The family have maintained a strong commitment to the company with a 72% stake. The company was nearly out of business only 20 years ago until CEO Marc Puig took control and has grown the business steadily since. In fact we value the near-death experience that still lives in the family and corporate memory. The company’s energy and focus are a result of that period and is evident through their growth being consistently ahead of peers.

Observations From The Road

During the quarter we spent time in both Europe and the US visiting founders and executives across fund holdings and new ideas as well as peers, suppliers, industry experts.

We met with Puig industry peers and former Managing Directors. The beauty industry is a steady consistent grower, but has been in a slower growth phase as consumers face cost of living pressures and China a big beauty market has faced its own economic pressures. Yet Puig continues to grow high single digits being in the sweet spot of prestige fragrances in developed markets. Fragrances is one of the more underpenetrated categories of beauty. Penetration is said to be 50% in Europe and <30% in the US. China is at 5%. Adoption and usage is growing, in particular amongst gen z. More so 6 luxury companies dominate the prestige fragrance category. The brand names are very sticky and enduring with Puig owning 3 of the top 10 fragrance brands. While the consumer is under pressure, a $150 fragrance is much more affordable than a handbag that costs thousands with the same logo. Puig is still skewed to Europe and the geographic build out in the Americas and Asia has a long runway.

We also spent time with many industrial companies and alternative asset managers across both Europe and the US. CEOs of large European industrials were expressing concern with the new tariff situation. Less so from a competitive dynamic but more from a sense they are seeing in real time the uncertainty causing a pause in decision making. As one CEO said “We are now being quoted on a cost-plus tariff surcharge which is who knows what. I can’t go to my board with that for new investments”. Most need some certainty to keep moving their businesses forward. While the general industrial environment was more cautious with the uncertainty, energy investment and in particular gas and LNG is an area of excitement and investment. Large European industrial businesses that were champions of electrification are talking about the inability for renewables to fill the energy need and the role gas will play. The Funds investment in Hess Midstream and Aker ASA have benefited from this improved sentiment.

The tariff situation is ever evolving, and we will attempt to remain flexible should the outlook shift one way or another. What we do know is in the more challenging operating environments; the top operators can really differentiate themselves in their markets. Changing supply chains and managing inflation is not an easy task and the good ones will further enhance their competitive positions and leadership. We saw this back in 2016 with the China tariffs and again expect the best companies and management teams/owners to separate themselves again.

Portfolio Snapshot

Past performance is not a reliable indicator of future performance

Source: Internal CI data reports, March 31, 2025

Top 5 Fund Holdings

| Name | Region | Capital Pool |

|---|---|---|

| Brookfield Corporation | North America | Real Assets & Income |

| Brown & Brown, Inc. | North America | Compounding |

| Constellation Software Inc. | North America | Compounding |

| Royalty Pharma Plc Class A | North America | Real Assets & Income |

| Investor AB Class B | Europe | Real Assets & Income |

Regional Exposure

Capital Pools

Sector Exposure

Since Inception Net Returns in Up/Down Markets

Portfolio & Risk Metrics

| Portfolio | Benchmark | |

|---|---|---|

| Price/Earnings | ||

| Yield | ||

| Price/Book | ||

| Net Debt to Equity | ||

| FCF Yield FS | ||

| Forecast Earnings Growth | ||

| Return on Equity | ||

| Tracking Error | ||

| Beta |

Further Information

Looking for further information regarding the Fund, please don’t hesitate to get in touch: