Performance Summary

Past performance is not a reliable indicator of future performance

Source: Internal CI data reports, March 31, 2026

Inception Date: 1 September 2008

*Annualised

¹Past performance is not a reliable indicator of future performance.

Portfolio Observations

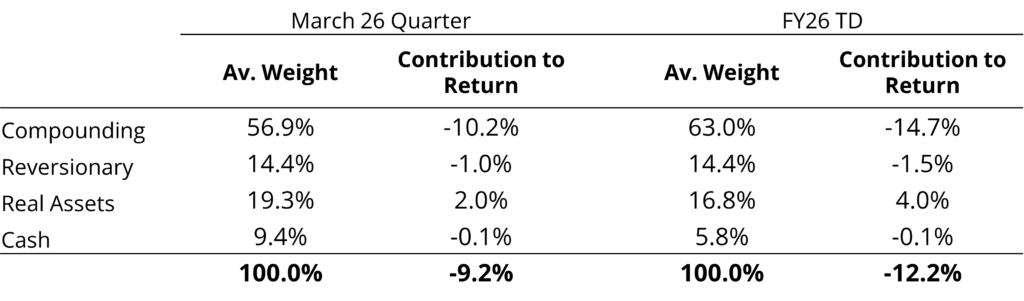

Compounding Capital Pool

These are the “generals” of the portfolio - companies with clearly defined customer propositions, observable growth runways backed by industry tailwinds, attractive financial models and run by aligned management teams with deep domain expertise. Investment returns are earned as the businesses execute on multi-year strategies, driving growth in sustainable Free Cash Flow per share and hence a “compounding” of shareholder value.

For most of the last decade these sorts of investments have been an attractive hunting ground for listed market investors. The archetypal compounders are capital-light, such as software or data vendors, marketplaces and services businesses. This capital-light element effectively supercharges the compounding potential.

Where the debate around Freee is about long-run business model durability, the investment case for Ryan Specialty (RYAN), the other significant detractor for the period, has been tested by something more traditional - a turning insurance cycle. The question of AI's impact on wholesale broking is not lost on us, but we believe that the weakening insurance pricing environment has been more impactful on investor sentiment to date.

As described by Founder and Executive Chairman Pat Ryan on the 2025 Q4 earnings call, "What distinguishes this cycle is simple. It was harder for longer on the way up and much faster on the way down, particularly as it relates to property." Pat went on to share that in more than 60 years in the industry he has rarely witnessed market sentiment shift this rapidly. We also failed to recognise how quickly the cycle was turning — or more directly, we failed to at least reduce the size of the investment as the operating environment was clearly softening. Ryan Specialty's competitive position remains strong, and management continue to invest countercyclically in talent and technology. However, given the continuing weakness in end markets, we have materially reduced the size of our investment.

Reversionary investments are predicated on the concept of mean reversion, but with observational evidence that the reversion will occur. Certain cyclical sectors may fall into this category. More often we look for company specific opportunities where cash flows are obscured but we can observe a pathway for this latency to be unlocked. Archetypes include spin-offs, low-risk turnarounds or businesses transitioning from a period of heavy investment to cash flow harvesting. These investment returns are typically uncorrelated to the rest of the portfolio as they are driven by company specific execution.

Today our reversionary holdings are largely in businesses inflecting from investment to free cash flow generation. For example, US broadband company Shenandoah Telecommunications (SHEN), which is on the cusp of completing a multi-year fibre deployment.

Real Assets are investments backed by hard assets that we expect to hold their real value over the long-term, particularly through periods of inflation. We strictly avoid assets with excessive leverage, as this would undermine the “real” nature of the investment. At certain points in a cycle Real Assets will perform very differently to the other pools, and should provide a source of capital for redeployment into Compounding or Reversionary opportunities.

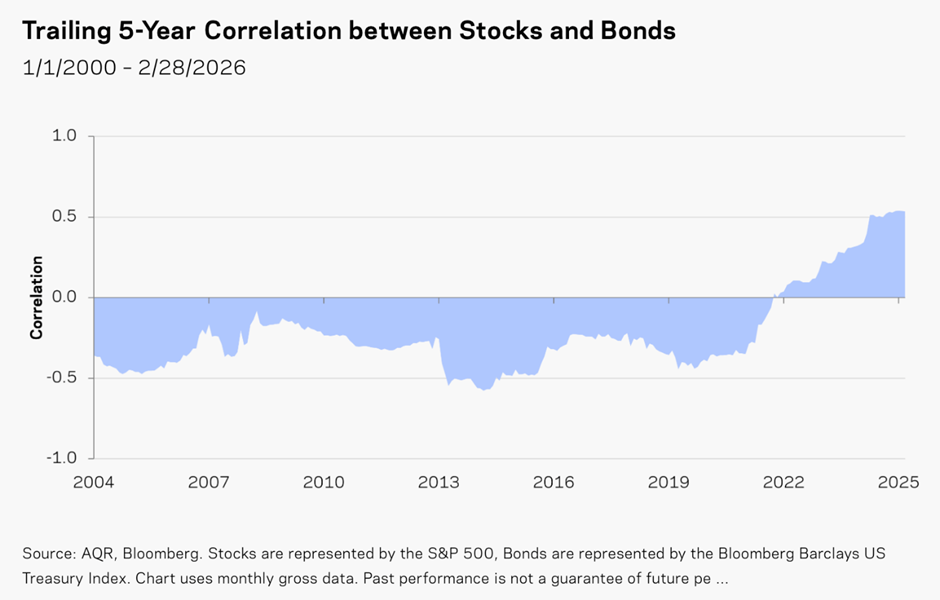

We anticipate that this capital pool will play an increasingly important role over the coming years. In March the Financial Times² discussed the positive correlation between equities and bonds which resulted in “global stocks and bonds have this month suffered their biggest combined sell-off since 2022 as the energy shock unleashed by the Iran war leaves investors “nowhere to hide”.

The result of this combined sell-off has been a poor outcome for the traditionally structured 60:40 portfolios. As the FT article states “the combined moves have put a traditional “60-40” portfolio of equities and bonds on track for the worst month since September 2022, when a previous cycle of global interest rate rises hammered markets. Even gold has tumbled as investors rush to liquidate previously winning trades, underscoring a lack of safe havens in financial markets.”

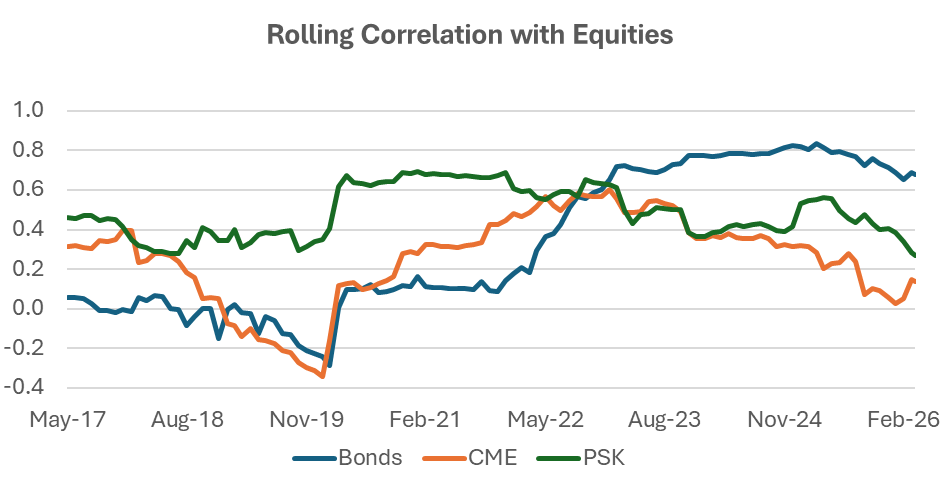

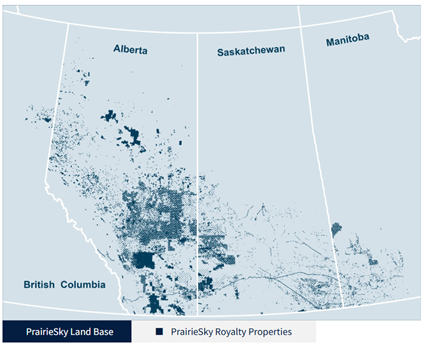

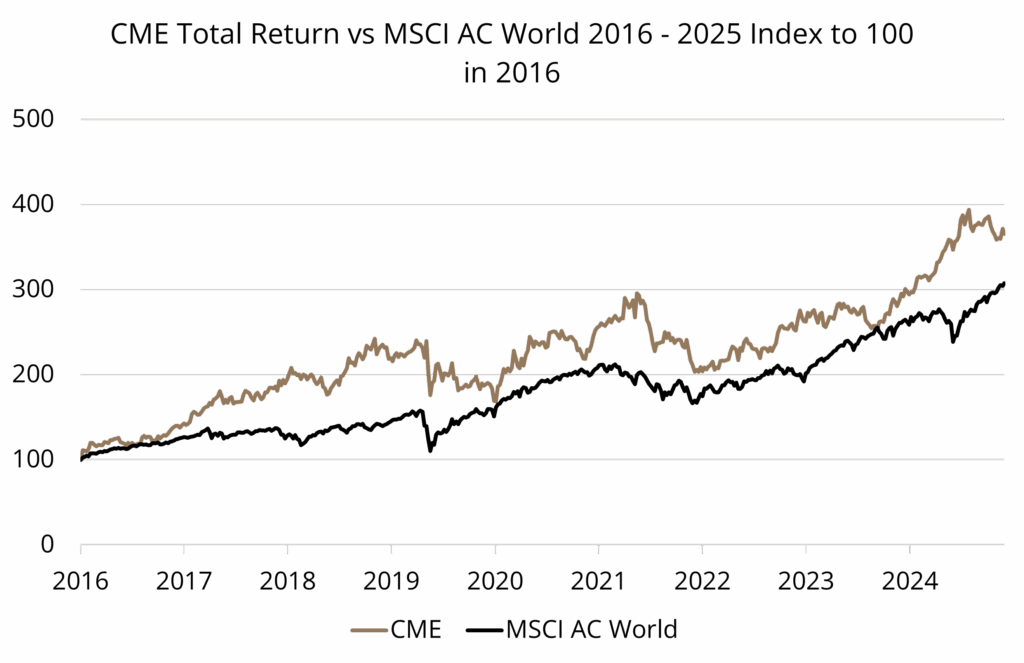

We think the key to identifying an effective alternative is to understand why the relationship has broken. The driver of this unwinding has been inflation. This can be hedged by real assets, for example the Fund’s holdings in PrairieSky Royalty (PSK) (a perpetual energy royalty owner over significant lands in the Western Canadian Sedimentary Basin (see Appendix 1)) and CME Group (the largest global derivatives exchange operator – an effective royalty on financial speculation, hedging and asset inflation (see Appendix 2)).

To further drive home the point, the correlation of bonds with equities started increased along with inflation in 2022, at which time the correlation of CME and PrairieSky started to decline.

Source: CI Analysis, FactSet. Bonds is a 50/50 split of US/International Aggregates. Equities = MSCI AC World. Analysis uses Total Returns.

² Stocks and bonds slump in tandem as Iran shock leaves investors ‘nowhere to hide’ FT 28 March 2026Appendices

Appendix 1

“Time is the enemy of a bad business, but a friend of a great business. As time melts away, dividends are paid, the business grows and the share count declines”. – Andrew Phillips, CEO of Prairie Sky Royalty

- Deep technical skills: they understand the most attractive resource opportunities, where the hidden and emergent value lies.

- Intuitive understanding of value creation: a deep, intuitive understanding of the option value that drives royalty value.

- First principles thinking: spend most of their time alone studying, charting their course for which they are laser focused.

- Patient, counter cyclical investing: able to behave counter-cyclically; being patient for long periods and then moving aggressively when opportunity present (we would suggest it’s hard to achieve this without also demonstrating the first three).

At the 2025 Investor Day in May, PSK provided an update on the value of their royalty asset base. This value, albeit undiscounted, stands at circa C$30B as compared to PSK’s current Enterprise Value of less than C$6B.

“No value is assigned…expansions of productive trends, enhanced oil recovery, better type curves with technology, and the discovery of new pools. This…is why I own the company.” – Andrew Phillips

²Please note that this is a forecast only, based upon Cooper Investors’ current views and assumptions, and is not guaranteed to occur. Any forecast may differ materially from the results ultimately achieved.

Appendix 2

Focused Management Behaviour

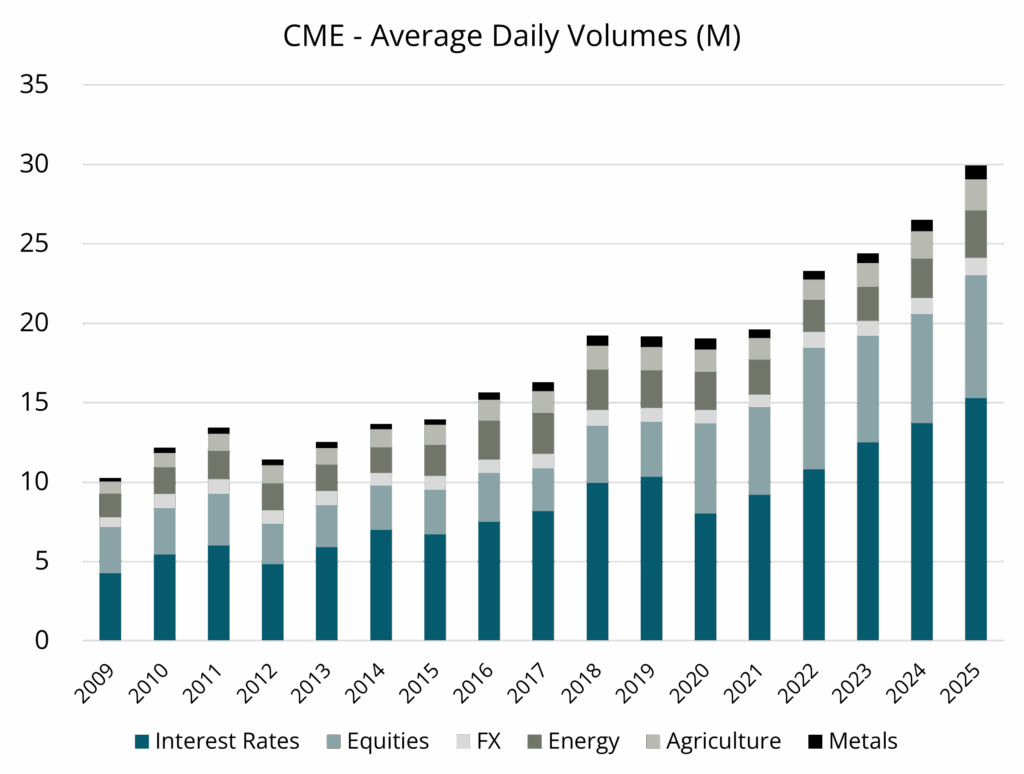

CME revenue base is diversified across six key asset classes (with Crypto an emerging seventh). Products across the key areas include derivatives over:

Interest Rates – US Treasuries, SOFR, Fed Funds

- Equities – S&P 500

- Foreign Exchange – JPY/EUR/GBP-USD

- Energy – WTI Crude, Henry Hub

- Agriculture – Corn, Wheat, Soybeans, Livestock

- Metals – Gold, Silver, Platinum, Copper, Aluminium

- Crypto – Bitcoin, Ethereum

Latency then stems from inevitable bouts of volatility which we note that in the current geopolitical and macroeconomic environment can be rapid, violent and frequent.

Portfolio Snapshot

Past performance is not a reliable indicator of future performance

Source: Internal CI data reports, March 31, 2026

Regional Exposure

Capital Pools

Sector Exposure

Market Capitalisation

Portfolio & Risk Metrics

| Portfolio | Benchmark | |

|---|---|---|

| Price/Earnings | ||

| Yield | ||

| Price/Book | ||

| Net Debt to Equity | ||

| FCF Yield FS | ||

| Forecast Earnings Growth | ||

| Return on Equity | ||

| Tracking Error | ||

| Beta |

Further Information

Looking for further information regarding the Fund, please don’t hesitate to get in touch: